Table of Contents

The Line Card Pulse is a quick, curated roundup of key news in furniture and lighting, turned into practical signals for revenue leaders and sales teams.

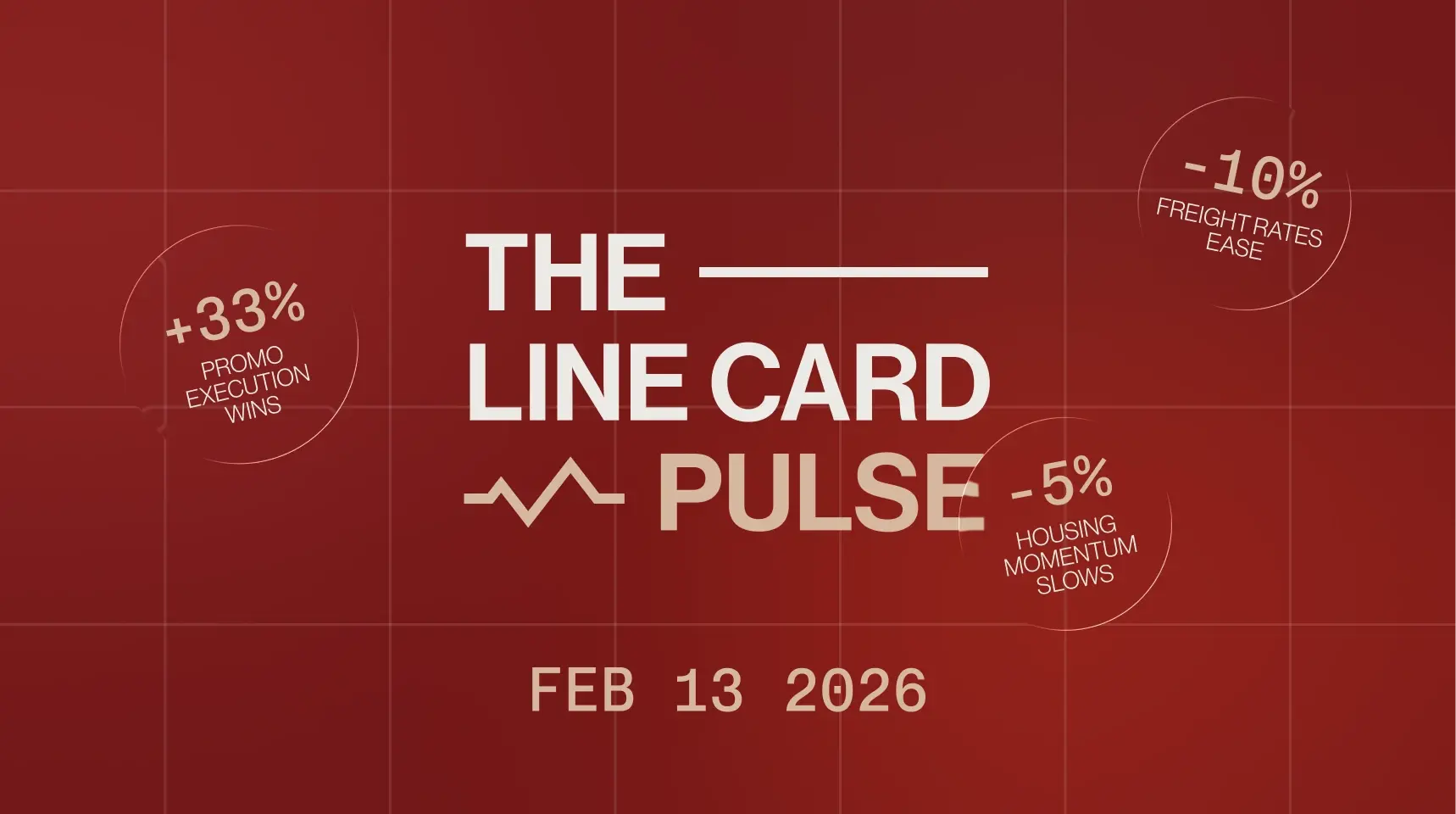

January's retail numbers told two different stories. One retailer watched traffic flatline while another posted double-digit gains. Same market, same week. The difference was execution timing during a three-day promotional window paired with financing clarity at checkout.

That gap is widening. Read the full digest below for specific signals, confidence levels, and sourcing.

Furniture Demand Shifts to Room-Level Upgrades

Housing starts are down roughly 4.6% month-over-month, and existing-home sales are forecast to grow only modestly in 2026, constrained by mortgage lock-in as 30-year rates hold near 6%. Despite this, furniture demand is holding in categories aligned with "stay-put" behavior. Orders are increasingly room-specific (living room, motion, and bedroom) rather than full-home furnishing tied to relocation.

Why it matters:

- Full-house furnishing cycles are becoming less frequent, reducing average order size and weakening the traditional link between housing turnover and furniture spending

- Product assortments must support modular, durable, and upgrade-friendly formats

- Sales forecasting models built on housing metrics are losing reliability.

Sources: U.S. Census Bureau, Furniture Today, NerdWallet

Promotional execution plus financing clarity drove January retail wins

Retailers that posted strong January results did so through clearly defined promotional windows paired with financing offers. Gains were concentrated during promotions rather than sustained baseline traffic growth.

Why it matters:

- Demand is conditional on promotional alignment; missed execution during key windows translates directly to missed revenue

- Inventory positioning and financing coordination become execution-critical, not secondary considerations

- Revenue volatility increases between promotional and non-promotional periods, complicating cash flow and capacity planning

Source: Furniture Today

Trade Channels Prioritize Suppliers Who Reduce Friction

Trade sentiment entering 2026 is cautiously positive, with most design and construction firms expecting a good year. At the same time, the majority expect product and material costs to rise, and roughly a third anticipate persistent labor shortages. Under this pressure, designers and builders are prioritizing suppliers with reliable lead times, transparent pricing, and dependable logistics.

Why it matters:

- Service reliability becomes a competitive differentiator equal to product design quality

- Brands with inconsistent lead times or unclear pricing risk quiet attrition from trade channel relationships

- Phased project purchasing means smaller initial orders but higher dependence on repeat performance and trust

Sources: Houzz/Furniture Today, Home Accents Today, Business of Home

Freight cost relief creates margin optionality for prepared operators

Global container spot rates declined approximately 10% week-over-week to around $2,212 per 40-ft container, reflecting muted post-holiday import demand and inventory digestion. Cost relief is real but time-bound.

Why it matters:

- Static landed-cost assumptions can misprice products or misallocate margin as rates shift

- Operators who lock in favorable rates can protect margin without needing to discount

- Organizations with slower cost update cycles miss the window entirely and see no financial benefit

Source: Furniture Today

Labor-market softening reinforces consumer caution

Private employers added only 22,000 jobs in January, well below expectations, with 57,000 losses in professional and business services and continued manufacturing declines. While not a collapse signal, the data reinforces consumer caution around discretionary, big-ticket purchases. Official BLS data is pending.

Why it matters:

- Big-ticket purchases become more sensitive to financing availability and perceived value

- Sales cycles lengthen as consumers delay commitment decisions

- Planning assumptions built on macro "rebound" narratives carry increased execution risk

Source: CNN/ADP

Read more insights

Smarter Selling Starts in Your Inbox

Get exclusive playbooks, guides, and case studies delivered monthly